De-risking Options

Brookfield Annuity offers companies and DB pension plans of varying sizes a range of options for managing and minimizing risk through group annuity buy-outs, group annuity buy-ins and longevity insurance. We’ll work with you to determine the best choice for your plan.

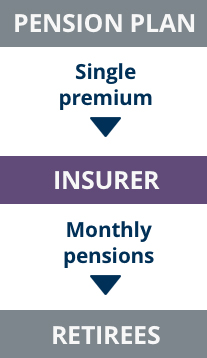

Group Annuity Buy-out

A group annuity buy-out allows DB plan sponsors to take the long-term risks and obligations associated with a specific group of pensioners and comprehensively transfer them to Brookfield Annuity.

Group annuity buy-out specifics:- A single premium payment made by the pension plan to the insurer – the “buy-out” – covers the designated group permanently.

- Brookfield Annuity then takes on the responsibility of providing full pension support and administration, which includes making guaranteed monthly payments to pensioners in the buy-out group.

- A group annuity buy-out involves a wholesale transfer of risk – both investment and longevity – and requires an accounting settlement. If a plan is underfunded, a top-up sponsor contribution will be needed to ensure that the portion of DB pension risk being covered is completely funded when the transfer is made.

- A group annuity buy-in, which does not need any accounting settlement, can be a first step to a group annuity buy-out.

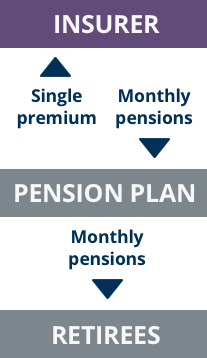

Group Annuity Buy-in

A group annuity buy-in is a solution that effectively transfers pension risk for a designated group of pensioners to Brookfield Annuity. It does not require either an accounting settlement or a contribution top-up.

- With a buy-in, the pension sponsor makes a single premium payment to Brookfield Annuity from the pension plan, which then makes guaranteed monthly payments back to the plan.

- Brookfield Annuity assumes the responsibility and the risk for making investments and payments, but the pension plan continues to be administered by the plan sponsor and the pension plan continues to make monthly payments to retirees.

- While investment and longevity risk is transferred through the buy-in, the plan still remains on the plan sponsor’s balance sheet, where the policy with Brookfield Annuity shows as an investment, and the sponsor also continues to administer the plan.

- A group annuity buy-in, which does not require an accounting settlement, can be a first step to a group annuity buy-out.

Longevity Insurance

Longevity insurance is an effective solution for managing the risk associated with increased longevity among a defined group of pension plan members.

People are living healthier and living longer. Since 1901, according to the Office of the Superintendent of Financial Institutions*, the average life expectancy of Canadians has increased by 33 years. That’s a wonderful thing, but it can have a significant impact on pension plans that were established with expectations about longevity that are no longer valid. Longevity insurance offers DB plan sponsors a practical approach to addressing longevity risk.

A plan sponsor makes fixed payments to Brookfield Annuity based on the expected lifespan of a designated group of pensioners. In return, we make variable payments to the pension plan based on the actual lifespan of pensioners within this group.

After purchasing longevity insurance, a pension plan retains the other risks associated with pension benefit payments.

*“Living to 100…will the Canada Pension Plan be sustainable?”, OSFI, October 2014